Lots of needlessly battle effectively selling insurance coverage due to the fact that of a collaboration with a bad insurance coverage company. Beware! Everybody with a pulse is hired in the insurance coverage organization! How does this impact you? It implies that the majority of firm recruiters stop at nothing to offer you on how fantastic their opportunity is. For that reason, it's VITAL that YOU talk to the insurance firm, as much as they interview you. Let's say you work for New york city Life or Northwestern Mutual. Or you're looking at joining a multi-level marketing business. My suggestion is to invest more of your attention on who your direct upline/manager is. Why? He is the one accountable for your success.

What are they like? Friendly, major, jerks? Additional reading If at all possible, get lunch with them to discuss their experiences. Ask your thoughts on how to begin selling insurance coverage. You might even consider asking to do a ride-along to see how the organization is like in front of prospects. Try to discover how the branch workplace helps develop you into a top-producing agent. Bottom line, local support from your agency and your direct upline/manager is critical for your brief- and long-lasting success. Without assistance, odds of failure boost significantly. Often times, agents I have actually recruited grumble about their past training and support.

The very best companies take no offense to any difficult questions you ask. In reality, they'll appreciate your thoughtful concerns due to the fact that you show both awareness and severity about wishing to find out how to start offering insurance coverage. When you choose which agency to sign up with, you should commit 100% to your task selling insurance coverage effectively. There's a terrific person that you ought to subscribe to on You, Tube. The channel is called Christopher Westfall, which also is this individual's name. I briefly discussed him in "Part 5" of this guide. He is a Medicare supplement extraordinaire. He understands the Medicare organization up and down.

He is a multi-millionaire many times over since of his dedication to this organization. He talks typically about how people in this organization stop working out because they don't fully devote. They have a Plan B. For example, they have actually got a spouse that makes a sufficient earnings, so there is little need for the representative to perform at peak levels. If we eliminate our options, safe zones, and alternatives, we have no other option but to be successful. Otherwise, we end up in a position to where we fail out entirely. If you want any sort of success finding out how to sell insurance, you have to burn the bridges.

If you are searching for a partner to develop you into a top-producing insurance representative, take a look at my nationwide agency recruiting program for more information. Make certain to check out about my Representative Success Stories along with purchase 1 of my 3 best-selling insurance coverage books - What is life insurance.

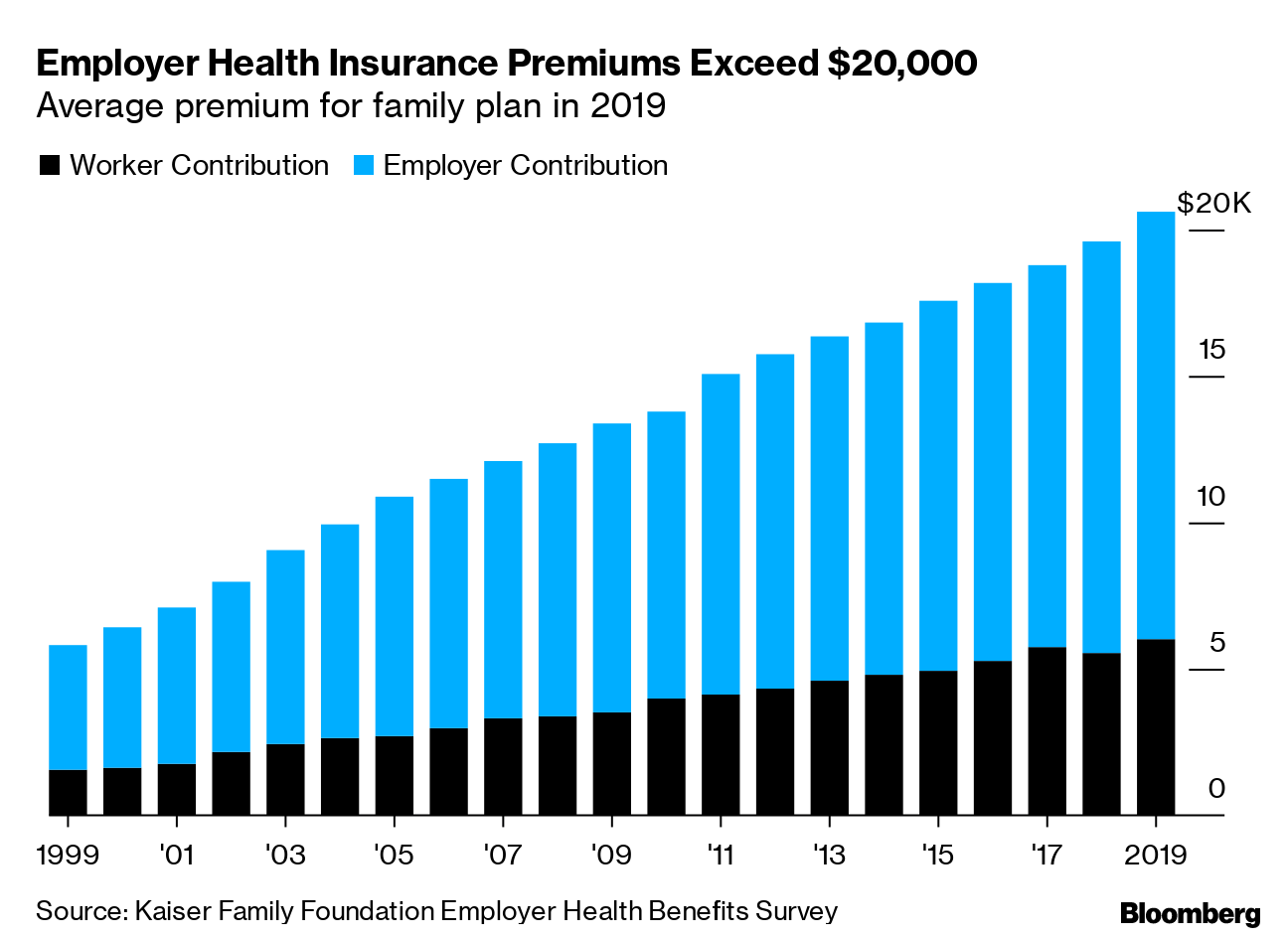

A Biased View of What Is Cobra Insurance

If you have a life insurance coverage policy you no longer desire or can't afford, stopping payments or simply cashing it in aren't your only options and even your best ones. Many individuals have offered their policies in a life settlement sale and come out the other side with money in hand but it isn't easy. You can transform your life insurance policy into money now, however the process is made complex. Initially, you'll need to have your life insurance policy evaluated to figure out the selling worth. Then, you'll need to discover a purchaser. When you have a purchaser in place, you'll receive a money settlement and the buyer will pay any premiums and collect the benefit when you die.

That is why lots of people select to either offer their policy to a settlement business or to a 3rd party through a life settlement broker. If you offer to a settlement company, you'll get a percentage of your policy's worth in money. If you use a broker, you might likewise pay a commission to the broker. However, a broker might have the ability to find a much better offer than you would on your own. There are a few things you need to think about prior to offering your policy. For instance:. Buyers might be trying to find Website link people over the age of 65 with chronic or terminal illnesses.

Your settlement could be based on income tax. If you're selling because you need money, you may have other alternatives, such as taking a loan versus your life insurance coverage policy, accelerating your payment date or selling the policy to a relative. However, bear in mind that these alternatives also have pitfalls and ought to be gone over with a financial consultant. Offering isn't all bad, specifically if you no longer desire the policy or you can't manage the premiums. If you do decide to sell, take these actions to ensure you get the most money: Your life insurance policy has guidelines about selling, and your state laws regulate the procedure.

If you don't fully understand, an independent monetary advisor can assist sort things out. There are no set worths for life insurance plan, and the deals you receive from purchasers can vary extensively. Evaluation numerous to make certain you're getting the best deal. Speak with an accountant to see what tax liability and eligibility modifications you will deal with after the sale. If you have large financial obligations, your creditors may have a claim to any cash you get from your life insurance settlement. If you have debts, discuss them with a financial advisor before you sell. The bottom line: If you don't desire your life insurance policy, it deserves a call to learn what you could get, however be careful about going through with it.

Disclosure: The details you check out here is constantly unbiased. However, we in some cases get compensation when you click links within our stories.

The Definitive Guide for What Does Liability Insurance Cover

Trying to find Click here to find out more a career that provides a big possible monetary benefit, a wealth of job opportunity, and the lure of self-employment? If you enjoy forging relationships and are dedicated to client service (and can deal with lots of rejection), insurance sales could well be for you. Insurance sales may be the ultimate commission gig, with its practitioners totally depending on their consumers' premium payments. Convert more potential customers. Get correspondingly richer. Repeat. A minimum of in theory. Being an insurance coverage salesperson is the ultimate commission gig; specialists are wholly depending on their consumers' premium payments. Insurance sales generally do not pay very well at first, but unlike those other professions, the longer you stick around in insurance coverage, the more earnings you make.

Like retail, customer support, and similar type of work with high attrition rates, insurance coverage sales normally don't pay all that well at the onset of one's career. Nevertheless, unlike those other occupations, the longer you remain in insurance, the simpler and more profitable it gets, thanks to recommendations and residuals. It's the remaining that's the difficult part. According to Pay, Scale, entry-level insurance representatives make roughly $44,700 in yearly settlement, consisting of bonuses, commissions and earnings sharing, and might not move up on the pay chart up until mid-career. If you're serious about offering life insurance for a living, here's one favorable.